In today’s volatile market, retail banks are compelled to rely on user data they have gathered in order to better satisfy customer’s demands. Accordingly, hyper-personalization in retail banking, which involves employing real-time predicted consumer demand data and analytics becomes crucial to expand or strengthen existing customer relationships and increase trust.

Table of Contents

Why is hyper-personalization imperative to retail banks?

According to Deloitte, hyper-personalization is the application of behavioral science and artificial intelligence to deliver products that meet each individual’s changing demands by collecting and analyzing real-time consumer data.

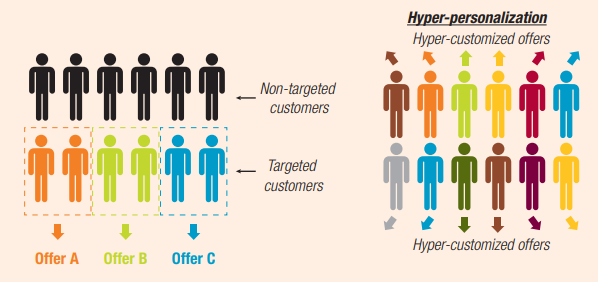

What is hyper-personalization? Source: storage.googleapis.com

Previously, retail banks tend to offer the same products and services to all kinds of consumers. However, at present, it has become an inevitable trend that retail banks personalize products and services to each customer, or practice hyper-personalization. There are two main drivers behind this shift: the increasingly complicated and diversified customer demands, and the significant growth of technology making hyper-personalization possible.

According to HSBC, customer service will form a new standard in the future as consumers demand highly personalized service that fully matches their unique requirements. Consumers nowadays are better aware and knowledgeable, and their requirements change day by day, striving toward individualized experiences (e.g. Consumers want retail banks to proactively send personalized offers and product information to them based on both their past interactions as well as anticipated future actions instead of general information). The bottom line is, unfortunately, that 94% of financial institutions are still unable to deliver on the “personalization promise”.

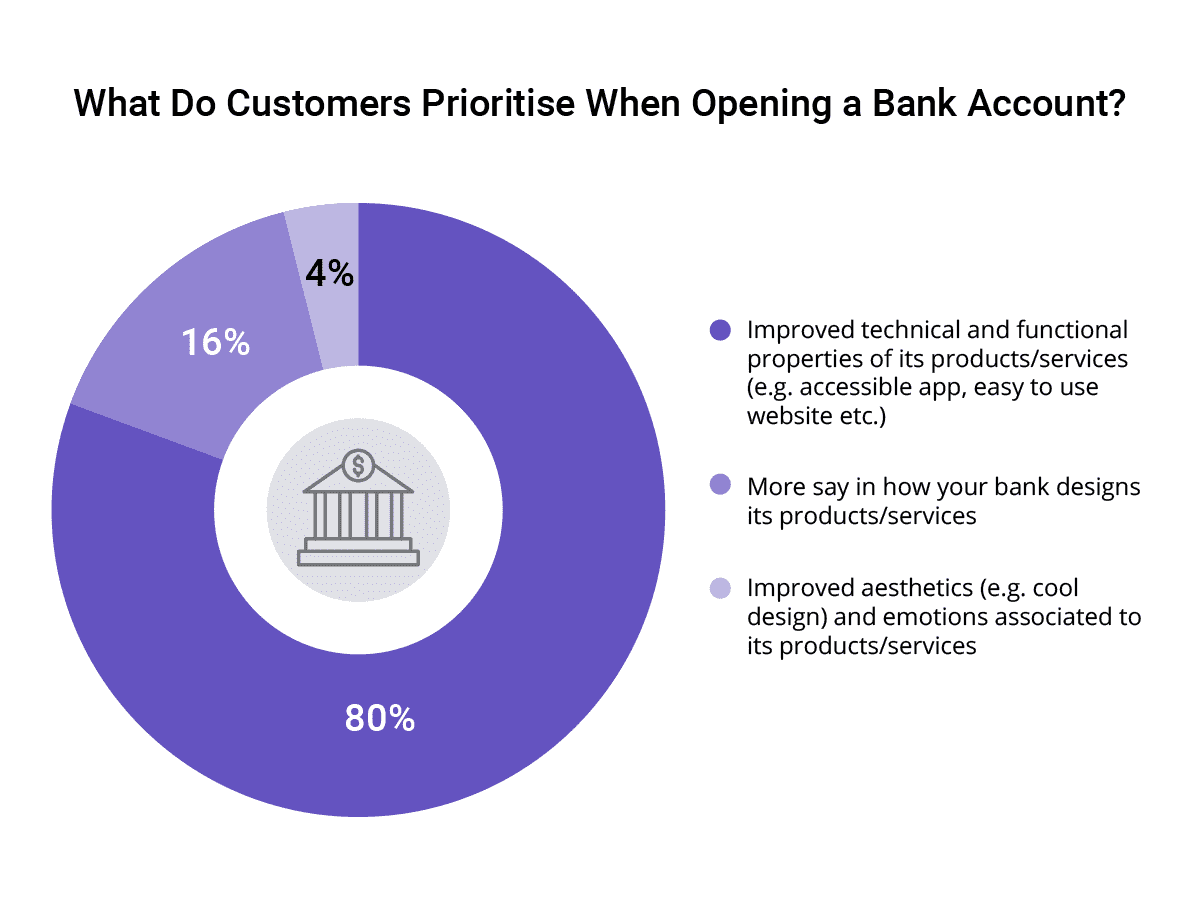

According to Deloitte’s report, when opening a bank account:

- 80% of customers prioritize banking products/services’s improved technical and functional properties (e.g.accessible app, Website that is simple to utilize, etc.);

- 16% of customers are interested in the way banks design their products/services;

- 4% of customers care about banking products/service’s improved aesthetics (e.g. cool design) and emotion.

Therefore, if retail banks can’t identify particular customer requirements as described above and focus only on selling products, they will almost certainly be unable to address customer demands.

Personalizing customer engagement is one of 5 Key Takeaways From 2021 Retail Banking to get accelerated in 2022. Discover more here!

Customer’s priorities when opening a bank account. Source: softjourn.com

Also, we have reached the digital era, where the necessity to store and analyze data sources is becoming increasingly important. It means that retail banks should recognize the potential of their gathered data and find a way to fully utilize that data. Data-driven strategy allows retail banks to identify consumer demands and requirements in real-time. Then, they can alter strategies and plans to better satisfy their customers.

In reality, retail banks will have a rich source of data since customers have expanded their engagements with their banks in many touchpoints and channels in recent years. Furthermore, in the next ten years, there will be the creation and development of digital IDs-records containing all personal information about finances, preferences, and consumption behaviors. Consumers will have individual ownership of their own data and the ability to decentralize who has access to their personal data. The more customers, who are willing to share their individual information, engage with their banks, the more data the bank can gather.

Besides, following years of focusing on digital transformation investments, retail banks have made significant technical improvements. Technology applications also demonstrate the bank’s capacity to use and benefit from their gathered consumer data.

Learn more about digitalization in Banking – Finance sector and akaBot’s solutions here.

How retail banks can benefit from hyper-personalization

Banks will differentiate their brand, enhance financial inclusion and boost revenue by implementing hyper-personalization.

To differentiate themselves

Customer experience is expected to overtake pricing and product as a firm’s brand differentiation. Customers increasingly want more complicated, faster engagements, as well as a tailored and consistent customer journey across channels and touchpoints. As a result, they are willing to provide personal information in exchange for a service that satisfies their specific requirements.

Through real-time data gathering and storing, smart devices have enabled retail banks to improve their customer service and customer engagement. However, retail banks cannot meet complex consumer requirements just via real-time data collection and storage.

Retail banks will definitely recognize that hyper-personalization is the “silver bullet” to differentiate themselves in a fierce bank competition. Behavioral science and artificial intelligence will help in the real-time analysis and processing of gathered data. As a result, retail banks can clearly define every-single customers’ requirements, even foresee their latent demands, then they can be able to fully satisfy their customers’ requirements immediately.

To improve financial inclusion

Financial inclusion, according to the World Bank, means that individuals and businesses, particularly the low-income and vulnerable, have access to appropriate, convenient financial products and services at reasonable rates. If retail banks want to expand their customer base, they should improve their financial inclusion, which means offering adequate financial products and services to all customers, even those with low incomes. Underbanked customers are not suitable with banking products and services that are:

- Charged at unaffordable or poor value-for-money prices;

- High risk-management requirement;

- Complex (i.e. difficult to understand).

To handle these customers, retail banks must understand their demands and abilities. Hyper-personalization allows retail banks to clearly understand the demands of each individual customer, even underbanked customers. From there, retail banks may adjust existing products and services or develop new products and services to each consumer group.

To boost revenue

Retail banks benefit from hyper-personalization in the race to gain market share, attract new customers, and retain existing ones. According to Deloitte, a firm’s revenue tends to improve after implementing hyper-personalization in a certain level of adoption. Specifically:

- Amazon and Netflix derive 35% and 60% of their revenue from hyper-personalized recommendations,

- Starbucks Revenue triples through redeeming hyper – personalized offer redemptions.

As per Deloitte, hyper-personalization is financial leverage that enables retail banks to generate new sources of profitable revenue to compensate for revenue lost due to changes in regulations governing how banks charge fees for products and services.

The benefits that retail banks get when implementing hyper-personalization. Source: benefiz.fr

Hyper-personalization enablement strategy

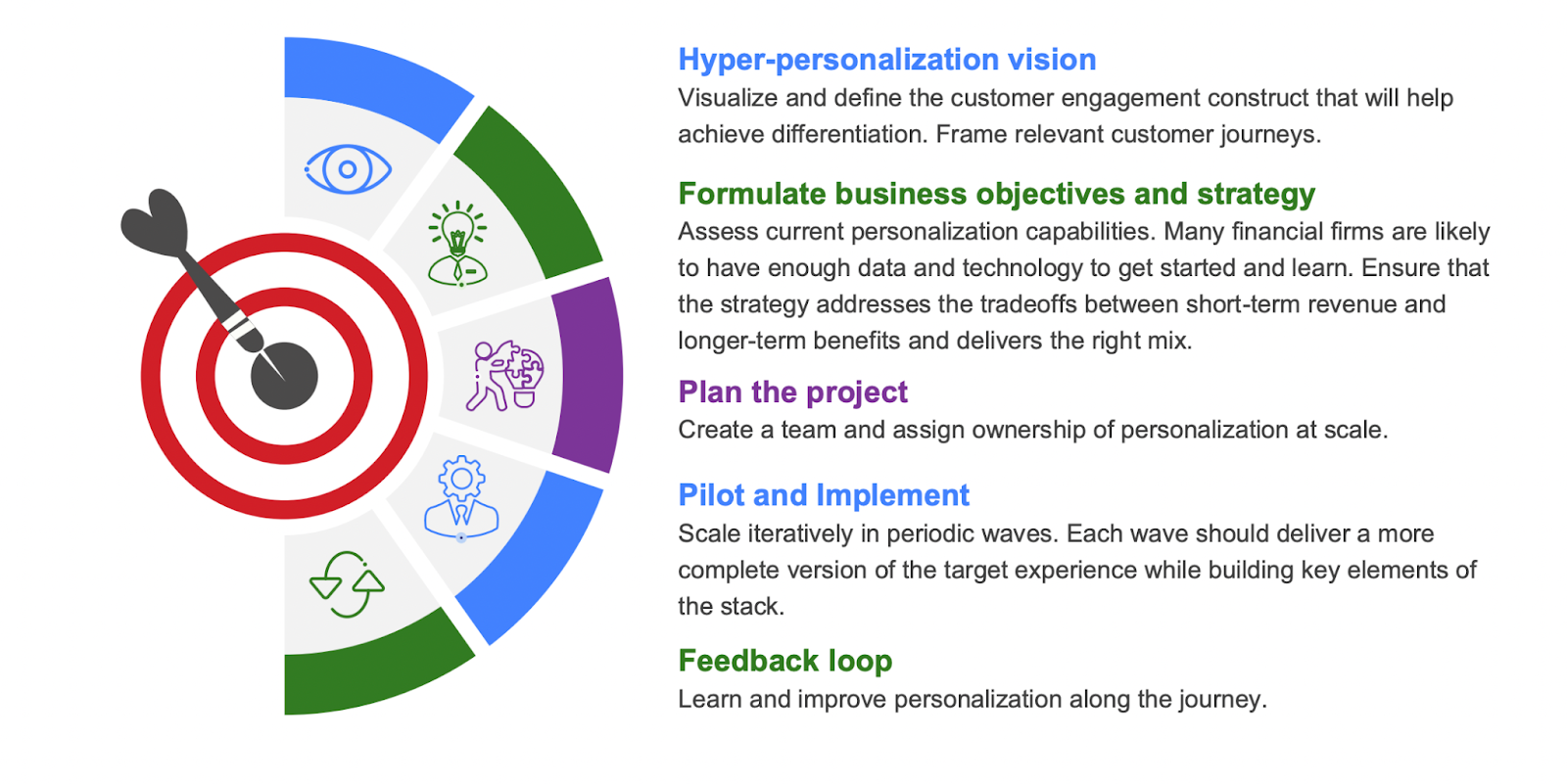

According to a Wipro’s report, in order to develop a comprehensive hyper-personalization capability at retail banks, the appropriate strategy for adopting hyper-personalization concepts must be applied systematically and through a series of steps.

5 stages of hyper-personalization strategy in retail banks. Source: wipro.com

- Stage 1 – Establishing a “vision of hyper-personalization”: First and foremost, retail banks should visualize and design their customer engagement framework. The retail bank then sets up suitable customer journeys.

- Stage 2 – Defining business objectives and strategies: At this stage, retail banks should assess their current hyper-personalization capabilities. In terms of data systems and technologies, several retail banks are qualified to begin applying hyper-personalization. Many banks, however, fail to reach this criteria. Furthermore, retail banks should explicitly clarify strategies that assure both short-term revenue and long-term benefit objectives, as well as a harmonic blend of these two main objectives.

- Stage 3 – Hyper-personalized project planning: Detailed project planning is the cornerstone for guaranteeing project effectiveness and, as a result, outstanding target completion. Retail banks can form a specific team which is responsible for hyper-personalization projects.

- Stage 4 – Project piloting and implementation: Retail banks should test the hyper-personalization project on a limited basis before applying on a large scale. Simultaneously, retail banks should conduct a series of consecutive pilots in order to directly experience and identify both the effective and ineffective factors. Finally, the retail bank will launch the project’s most complete version.

- Stage 5 – Collecting and analyzing feedback: During the hyper-personalization project’s implementation, retail banks should gather and analyze feedback from multiple sources (including staff, customers, and so on) in order to maximize their hyper-personalization.

Sources:

Hyper Personalization in Financial Services – A Wipro Report

The future of retail banking – The hyper-personalisation imperative

Hyper Personalization: the next phase of banks’ digital evolution

How Is Hyper-Personalization Changing the Banking Landscape?

94% of Banking Firms Can’t Deliver on ‘Personalization Promise’

akaBot (FPT) is the operation optimization solution for enterprises based on RPA (Robotic Process Automation) platform combined with Process Mining, OCR, Intelligent Document Processing, Machine Learning, Conversational AI, etc. Serving clients in 20+ countries, across 08 domains such as Banking & Finances, Retails, IT Services, Manufacturing, Logistics…, akaBot is featured by Gartner Peer Insights, G2, and ranked as Top 6 Global RPA Platform by Software Reviews. akaBot also won the prestigious Stevie Award, The Asian Banker Award 2021, etc.

Leave us a message for free consultation!