BaaS (Banking-as-a-Service) is considered a new trend, especially when several businesses and retail banks focus on promoting a digital ecosystem, integrating with products and services of partners to increase convenience and experience for customers. So what is BaaS, and what values does it bring to retail banking? Opportunities and challenges of banks when implementing BaaS in Vietnam? The article below will provide a comprehensive guide on the topic.

Table of Contents

What is Banking-as-a-Service?

Banking-as-a-Service (BaaS) is a crucial component of Open banking. In this model, the licensed banks open their APIs (Application Programming Interface), allowing their core financial services to integrate directly with the products of the non-banks. In other words, non-banks or fintechs develop products on top of regulated banking infrastructure. This opens the door for businesses to build new financial services, provide additional convenience, and build a comprehensive ecosystem for users.

BaaS helps banks to enter new markets and diversify financial services. Source: blog.withplum.com

For example, an airline wants to provide customers with online payment service and a payment card so that customers can gain reward points for each purchase of airline tickets via the card. However, to do this, the airline needs to have a banking license or licenses related to the provision of banking services. Typically, the licensing procedure is complicated, particularly businesses that are not in the banking sector. Therefore, BaaS is considered as the solution for the above problem. The airline could work directly with the licensed bank providing the BaaS platform in exchange for using the bank’s services through the API. Then, the airline could build or develop a new product suitable for the target customers.

BaaS model often involves 3 main components:

- Banks: A licensed bank enables other businesses to integrate the bank’s core banking services into their products/services via APIs.

- BaaS Platform: BaaS is API-based that provides software to ensure secure data communications between the bank and the business.

- Businesses (Fintech/non-fintech): These are the actual customers of the BaaS providers. Typically, fintech/non-fintech businesses use BaaS to build new financial services solutions for their customers.

Some major use cases of BaaS

Digital banking

BaaS facilitates fintech/non-fintech companies to provide online banking services to their customers. These advanced and user-friendly products can meet customers’ needs, such as handling accounts with high efficiency, switching accounts at will, etc.

Banks can integrate with enterprise systems to bring new financial solutions to customers through APIs. Source: sp-ao.shortpixel.ai

An example is a partnership between Abu Dhabi Islamic Bank (ADIB) and Fidor Bank. Fidor designed, tested, and built a digital banking project into a multi-service digital banking platform through APIs, providing a seamless and easy experience for Gen Y users, the target customers of ADIB.

Credit and debit card services

BaaS allows non-banking businesses to offer credit and debit cards to their customers. Customers can obtain real-time updates on all transactions through an app, resulting in faster, more efficient payments.

An example is Stash, a New York-based fintech company engaged in the BaaS model with Green Dot Bank. Green Dot uses an API, allowing a Stash bank account to be integrated into the Stash app, providing debit cards with no overdraft fees to customers and access to a network of free ATMs across the US.

Savings and investment services

Non-banks and fintechs adopt the BaaS model to help customers save and invest assets. In this way, the client’s savings and investment could be balanced and personalized at low-cost index funds.

For example, through a partnership with UK-based Starling Bank, Raisin UK, the UK-based savings platform has boosted savings services for customers. Accordingly, Raisin uses Starling’s APIs to create Starling accounts for customers, collect customers’ savings deposits and transfer them to partner banks, allowing customers to choose the best savings deals on the market, tailored to each individual’s needs.

The benefits of BaaS

For customers

Innovation is fostered by enabling non-banks to provide core banking services to customers, enabling them to access more intelligent and convenient products. Besides, since customers are increasingly knowledgeable and tech-savvy, they expect highly innovative products in technology. Therefore, applying the BaaS model allows businesses to innovate products and bring superior experience to customers.

For businesses

Since fintech and non-banking organizations can work directly with licensed banks to access to bank’s core financial services through APIs, they can provide new financial solutions to customers without a banking license.

Accordingly, these businesses can speed up operations, accelerate speed to approach the market, and innovate products without spending huge costs or resources to maintain legacy systems. The result is competition and an enhanced position in the market.

In addition, according to Accenture, 43% of customers trust banks to manage their transactions and data effectively. Therefore, businesses associated with banks can leverage trust and increase customer satisfaction while increasing the number of potential customers.

The partnership between the bank and the other business brings comprehensive benefits to both sides. Source: media.vneconomy.vn

For banks

By allowing the use of APIs to provide services, banks could reap significant profits, especially when BaaS becomes popular. In fact, up to 43% of banks prefer to charge a fee per API transaction.

Not only bringing revenue to the bank, but BaaS also helps save significant costs. Hence, the bank does not need to invest many resources for technology development or infrastructure. Instead, they fully take advantage of the existing service platform and expand products with partners to increase revenue and enable new sources of growth.

In addition, the cooperation with third parties also gives the retail banks the opportunity to gain customer insights, such as payment habits or financial needs. From there, the bank can improve services, create highly personalized products, offer product packages tailored to the consumer’s individual needs, and attract many potential customers.

Opportunity for Vietnamese retail banks to develop BaaS model

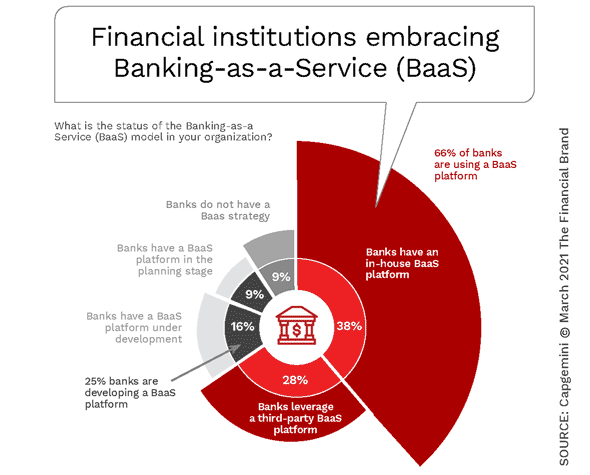

BaaS is considered an important trend in 2021 because the expansion of the BaaS model across the entire financial services industry creates favorable conditions for financial/non-financial institutions to create value and practical benefits for users. According to The World Retail Banking Report 2021 conducted by Capgemini and Efma, two-thirds of financial institutions use BaaS, and 25% are developing this platform. This trend has significantly increased the number of retail banks partnering with fintechs, technology corporations, and other non-banks to increase scale, create new products/services, reduce costs, optimize revenue streams, and gain customer insights.

Read more: 5 Key Takeaways From 2021: The Road to Success For Vietnamese Retail Banks

66% of banks are using BaaS, indicating the influence of this platform on the banking industry. Source: thefinacialbrand.com

The BaaS trend will continue to flourish in 2022, requiring retail banks to take steps to accelerate the growth of BaaS. One of them is the move towards “embedded finance”, which allows financial companies to embed services on other platforms using APIs. This would result in a diverse ecosystem, seamlessly connecting to different services such as social media, retail, transportation, hospitality, investment, and consulting services, increasing the potential to provide value to multiple customer segments.

In Vietnam, with young market potential, BaaS will have the opportunity to accelerate. This is because Vietnamese consumers increasingly prefer smart payment products that integrate a variety of digital services (data security, identity security), online shopping, flight booking, etc. According to the statistics of the State Bank of Vietnam, the growth rate of transaction volume via mobile banking in Vietnam is 200%; 77% are interested in digital banking and will experience this platform in future transactions (VISA survey on payment attitudes of Vietnamese consumers).

In addition, aware of the importance of applying innovative and creative technologies to the financial-banking sector, the State Bank of Vietnam has issued Decision No. 2655/QD-NHNN with the orientation towards 2025 would be the completion of a number of guidelines and policies for Open API. This is the legal framework and the premise for the proactive implementation of BaaS. This also means that the BaaS market still has room for establishment and development in Vietnam.

BaaS has great potential for development in the banking-finance sector in Vietnam. Source: encrypted-tbn0.gstatic.com

Therefore, retail banks need to be proactive in the journey to an open ecosystem, effectively implementing BaaS to speed up the digital transformation process in Vietnam, providing a superior experience for customers. When there is an opportunity, it is necessary to have the support of reliable consultants to prepare an effective implementation roadmap, creating a competitive advantage in the market.

However, despite many opportunities, as BaaS in Vietnam is at an early stage, Vietnam’s enterprises would deal with difficulties and barriers when applying new technology. One of the challenges banks have to face when implementing BaaS is security and confidentiality. Risks may occur when counterparties access the bank’s system through API, the illegal use of customer data, or when the customer makes a transaction on the new digital platforms. This requires banks to prepare scenarios to overcome risks in the deployment process, invest in technology infrastructure, ensure security, and promote state agencies to establish a safe, unified legal framework related to Open API and BaaS.

Discover more insights to get accelerated in digital transformation for the Finance – Banking sector here!

References

How The Banking-As-A-Service Industry Works And Baas Market Outlook For 2022

Banking As A Service, Reshaping The Financial Services Landscape

What The Hell Is Banking As A Service? And What Is It Not?

Banking-As-A-Service: Một Làn Sóng Mới

Banking as a Service: Meaning, Examples, Benefits and Future

Top BaaS Companies in 2022: Platform providers & banks using BaaS technology

9 Retail Banking Reflections and Keys to Success for 2022

akaBot (FPT) is the operation optimization solution for enterprises based on RPA (Robotic Process Automation) platform combined with Process Mining, OCR, Intelligent Document Processing, Machine Learning, Conversational AI, etc. Serving clients in 20+ countries, across 08 domains such as Banking & Finances, Retails, IT Services, Manufacturing, Logistics…, akaBot is featured by Gartner Peer Insights, G2, and ranked as Top 6 Global RPA Platform by Software Reviews. akaBot also won the prestigious Stevie Award, The Asian Banker Award 2021, etc.

Leave us a message for free consultation!